Section 80G Deduction – Income Tax Act

Section 80G deduction under Income Tax Act is available for contributions made to certain relief funds and charitable institutions. All charitable donations are not eligible for deduction under section 80G. Only donations made to prescribed funds qualify as a deduction.

Section 80G Deduction

The Government of India introduced Section 80G deduction to encourage people to donate by providing income tax relief. Under Section 80G, the amount donated is allowed to be claimed as a deduction at the time of filing income tax return. Deduction under Section 80G can be claimed by individuals, partnership firms, HUF, company and other type of taxpayers, irrespective of type of income earned.

Amount of Deduction under Section 80G

Donations paid towards eligible trusts/charities which qualify for tax deductions are subject to certain conditions. Donations under Section 80G can be broadly classified into four categories, as mentioned below.

Donations with 100% deduction (Without any qualifying limit)

Donations made under this category enjoy 100% tax deduction and are not subject to any qualification limit being met. Donations to the National Defence Fund, Prime Minister’s National Relief Fund, The National Foundation for Communal Harmony, National/State Blood Transfusion Council, etc. qualify for such deductions.

Donations with 50% Deduction (Without any qualifying limit)

Donations made towards trusts like Prime Minister’s Drought Relief Fund, National Children’s Fund, Indira Gandhi Memorial Fund, etc. qualify for 50% tax deduction on donated amount.

Donations with 100% deduction (Subjected to 10% of adjusted gross total income)

Donations made to local authorities or government to promote family planning and donations to Indian Olympic Association qualify for deductions under this category. In such cases, only 10% of the donor’s Adjusted Gross Total Income is eligible for deductions. Donations which exceed this amount are rounded off to 10%.

Donations with 50% deduction (Subjected to 10% of adjusted gross total income)

Donations made to any local authority or the government which would then use it for any charitable purpose qualify for deductions under this category. In such cases, only 10% of the donor’s Adjusted Gross Total Income are eligible for deductions. Donations which exceed this amount are capped at 10%.

Know more about donations qualifying for Section 80G deduction.

Documents Required for Claiming Section 80G Deduction

Taxpayers claiming deduction under Section 80G must have the following documents to support the claim.

Donation Receipt

It is mandatory to have a donation receipt issued by the Trust or Charity which received the donation. This receipt should include the following details mandatorily to be valid:

- Name and address of the Trust or NGO

- Name of the Donor

- Amount donated (mentioned in words and figures)

- Registration number of the Trust, as given by the Income Tax Department under Section 80G along with its validity.

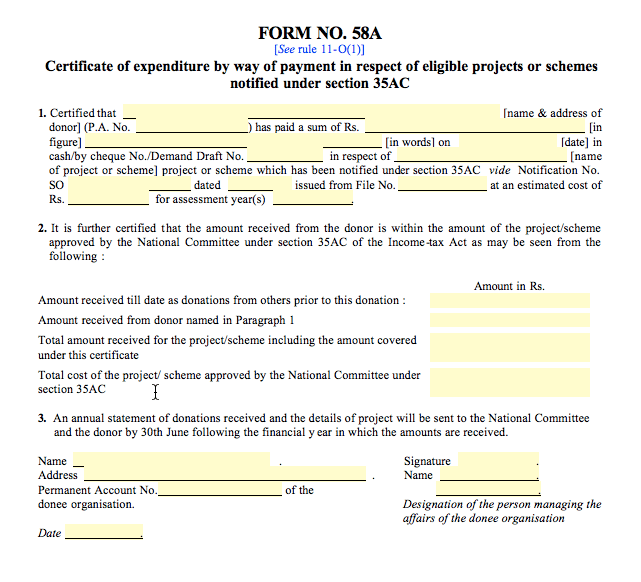

Form 58A

Form 58A is required if the taxpayers claims 100% deduction on a donation, without which their donation will not be eligible for 100% deduction. Form58A will be provided only for certain types of eligible deductions.

Comments

Post a Comment